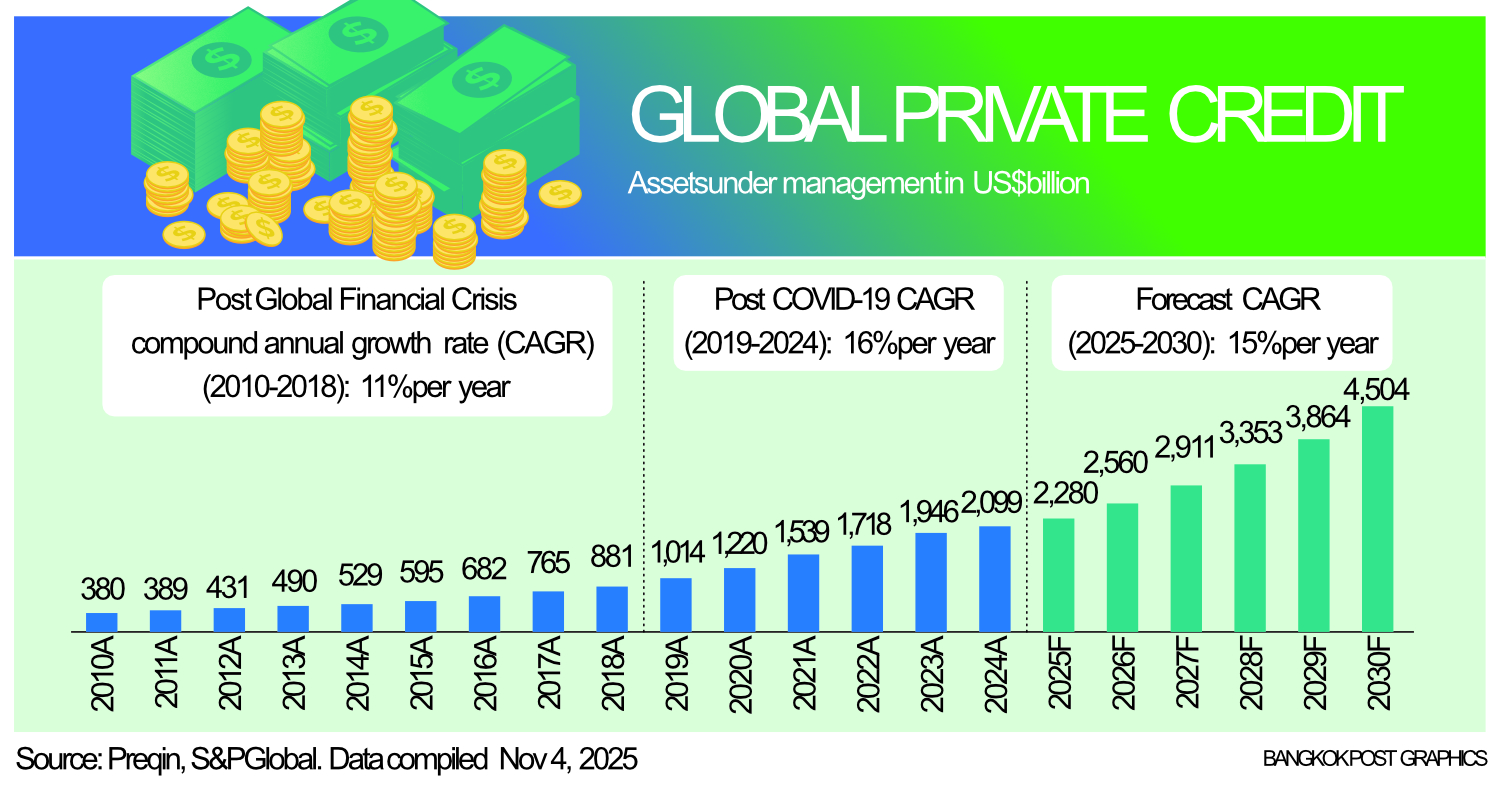

Private credit has rapidly expanded into a US$2.3-trillion global industry, raising questions about whether this growth represents genuine financial strength or early signs of a bubble. At the same time, interest in private credit in Thailand has increased significantly as companies search for new ways to access capital while traditional funding channels become increasingly restrictive.

Although it may appear relatively new to some market participants, private credit has been part of global financing for decades. At its core, private credit refers to lending provided by investment funds rather than banks. These lenders negotiate flexible structures, stronger protections and closer monitoring of borrowers compared with traditional bank loans or public bonds.

The asset class accelerated after the 2008 global financial crisis, when new regulations forced banks to reduce certain types of lending, especially to mid-market companies. During the Covid-19 pandemic, companies urgently needed liquidity while banks again became more cautious.

In both periods, private credit stepped in to fill the funding gap and gradually became a major component of the global financial system.

Today, with private-credit assets reaching $2.3 trillion, investors naturally ask: Is the market overheating?

Concerns intensified after the failures of two companies — Tricolor and First Brands — in the US. Jamie Dimon, the chief executive of JPMorgan, remarked: “If you see one cockroach, there are usually more.” This sparked fears of broader issues. However, deeper analysis shows these failures were company-specific problems, not systemic weaknesses in the private credit model:

- First Brands Group, an auto parts maker, held $9-10 billion in debt, mostly tied to syndicated loans, not private credit facilities.

- Tricolor, a specialist in lending to high-risk borrowers, failed due to alleged double-pledged collateral and inaccurate loan-tape reporting.

These incidents do not reflect the structure or discipline of mainstream private credit. In fact, private credit is known for tight covenants, strong collateral backing and active monitoring — characteristics also present in private credit in Thailand. These isolated failures should not be interpreted as systemic warning signs.

A SHIFT, NOT A BUBBLE

The global growth of private credit over the past decade reflects a structural shift in corporate financing rather than a short-term bubble. From 2014 to 2024, global private credit assets under management increased from $529 billion to $2.3 trillion, representing a compound annual growth rate of nearly 15%, significantly higher than the 6-7% growth for traditional asset management businesses.

Private credit has also delivered attractive performance, offering 8-12% annual returns and default rates near 2%, resulting in strong risk-adjusted outcomes.

Large global private credit platforms now manage hundreds of billions of dollars across corporate, real estate and infrastructure credit, demonstrating long-term institutional confidence. These global trends support the view that private credit in Thailand is part of a broader, sustainable financing evolution.

While the US and Europe debate whether private credit is overheating, Thailand remains in the early stages of its private credit development. The Thai market is growing not because of risky behaviour or excessive liquidity, but because traditional financing channels are tightening.

Historically, Thai companies relied heavily on bank loans and corporate bonds. Today both channels face meaningful constraints. Banks are dealing with rising non-performing loans, stricter capital requirements and slower approval processes. Meanwhile, the bond market has contracted noticeably.

According to the Thai Bond Market Association, corporate bond issuance declined 19% in 2023, fell 10% in 2024, and is projected to drop another 10-12% this year as investors shift towards stronger investment-grade issuers and become more cautious following several recent high-profile defaults.

This has created a structural funding gap, similar to conditions seen in the US in 2010, Australia in 2013 and Japan in 2017 — each of which experienced significant private credit expansion. Thailand is moving into the same phase, making private credit in Thailand increasingly important.

Thailand’s most compelling private credit opportunities today involve senior secured, asset-backed structures. These transactions are anchored by real collateral — such as real estate, machinery, equipment or infrastructure assets — and provide lenders with clearer repayment visibility and stronger downside protection.

These structures often incorporate strict cash-flow waterfalls, security over assets, control accounts, covenants and cash-sweep mechanisms. As a result, many private credit transactions operate similarly to enhanced fixed-income investments, offering predictable cash flows with stronger protection than traditional unsecured lending.

Private credit does carry risks, including valuation accuracy, enforceability of collateral, governance standards and cash-flow volatility. However, disciplined structuring, proper legal documentation and active monitoring can effectively manage these risks.

NEW FINANCING PILLAR

From the perspective of PrimeStreet Group, the continued growth of private credit in Thailand as a new financing pillar requires disciplined risk management — ensuring conservative collateral values, enforceable security packages, transparent reporting, strong governance and robust cash-flow protections through structured waterfalls and covenants.

With these safeguards in place, we believe private credit can become a responsible, resilient and enduring alternative source of funding that supports Thai corporate clients in growing their businesses and pursuing long-term expansion.

Rewin Pataibunlue is a Founding Partner and Group CEO at PrimeStreet Group, an investment banking, strategic management consulting and alternative fund management firm based in Bangkok.