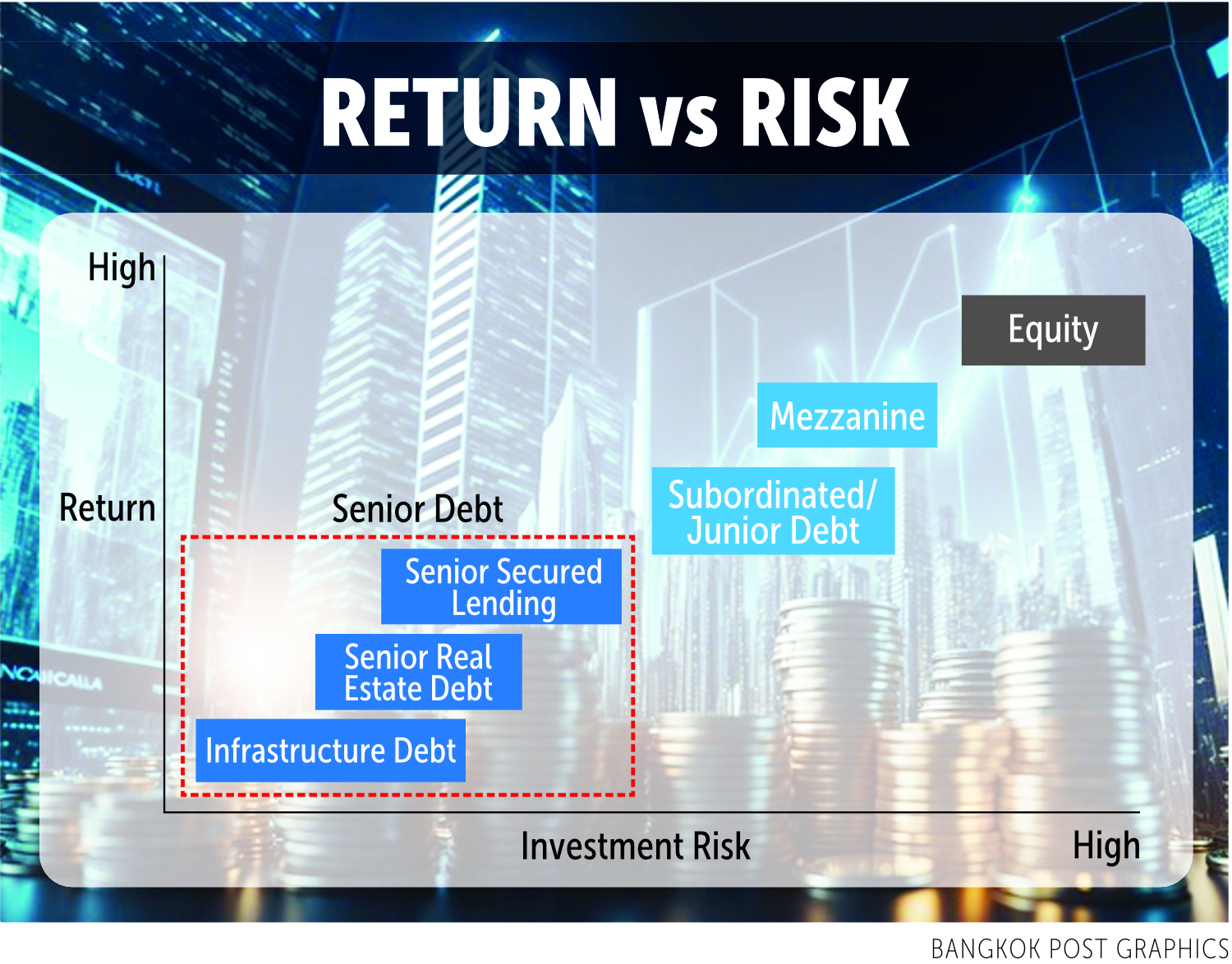

Private credit has quickly expanded from a niche strategy into a core allocation for global investors. The asset class offers stable income, negotiated protection and senior ranking in a borrower’s capital structure.

But as private credit becomes more widely adopted in Thailand, one message is critical: this is not a risk-free investment. Its resilience depends on discipline, structuring strength and the expertise of those who underwrite, monitor and manage each deal.

Before investors participate in this fast-growing market, they must understand the key risks that define private credit and how professionals mitigate them.

Illiquidity Risk: Illiquidity is among the most misunderstood risks in private credit. Unlike public bonds that can be traded daily, private credit loans cannot be exited easily. They are privately negotiated, non-tradeable instruments that are typically held to maturity or exited only under specific circumstances such as refinancing or sponsor buybacks.

Global private credit platforms operate closed-end funds with lives of 5-10 years. These multi-year structures are necessary to conduct deep due diligence, negotiate protections, monitor performance and execute controlled exits. They are built for stability — not liquidity.

The illiquidity premium is attractive only if investors understand the trade-off. Private credit is not suitable for those seeking quick liquidity or short-term flexibility. It rewards long-term commitment, where returns come from disciplined execution of a structure rather than market movements. Capital remains deployed until the loan matures, refinances or transitions through a planned exit.

Structuring Risk: Private credit’s true strength lies not in high coupons, but in structure. Well-designed structures protect principal even when a borrower’s business faces pressure. Poorly structured loans, by contrast, expose investors to unexpected losses.

Robust structuring typically includes clearly defined cash-flow waterfalls that prioritise debt repayment. Cash-sweep mechanisms automatically reduce leverage when performance exceeds expectations.

Enforceable collateral rights, backed by independent valuation and legal clarity, ensure that lenders can act decisively when required. Maintenance covenants serve as early warning signals, enabling lenders to intervene long before financial stress becomes irreversible.

These elements are engineered, not incidental. Senior secured credit facilities globally include liquidity thresholds, debt-service coverage tests, controlled bank accounts, receivable-flow monitoring and strict limits on new borrowings. When conditions deteriorate, it is the structure — not the headline interest rate — that protects investors’ capital.

In Thailand, where transparency standards vary and reporting quality differs by sector, structuring discipline is even more important. A strong structure can determine whether restructuring is orderly and recoverable, or whether capital is permanently impaired.

Collateral Risk: Collateral provides comfort, but only when lenders truly understand the asset. Not all collateral is equal, and not all collateral behaves predictably in stressed markets.

Disciplined private-credit lenders adopt conservative, downside-driven valuation methodologies. Collateral is regularly stress-tested based on recession scenarios, price volatility and liquidity conditions. Loan sizing is determined by what the collateral may realistically be worth under pressure, not by optimistic assumptions or book value.

In Thailand, this risk is especially relevant for real estate-backed financing and industrial assets lending, where market prices can deviate sharply from accounting values. Collateral protects only when it can be liquidated efficiently without destroying value. This requires sector expertise, conservative analysis and readiness to take control if necessary.

Strong collateral not only supports recovery, but also underpins repayment strategies whether through cash flow, refinancing, asset sales or sponsor support.

Valuation Risk: Private credit is valued using mark-to-model, not mark-to-market. This reduces volatility but increases opacity. Valuations depend on internal assumptions, comparable transactions and forward cash-flow estimates rather than live market pricing.

Smooth marks do not always mean stable credit health — they reflect limited trading, not absence of risk.

Investors must understand that model-based valuations can mask early deterioration. Conservative valuation practices, independent reviews and disciplined monitoring are essential to avoid valuation surprises if conditions worsen.

Concentration Risk: Private credit portfolios can become concentrated due to illiquidity, large ticket sizes and limited deal flow. Heavy exposure to a single sector, sponsor group or borrower type can magnify stress in a downturn.

This is especially relevant in Thailand, where several sectors such as real estate, construction materials and certain small business segments experience cyclical volatility. A concentrated portfolio may perform well in stable periods but face correlated losses when a sector weakens.

Disciplined managers diversify exposures, monitor correlation risk closely and avoid excessive reliance on any one sector or borrower group. Diversification is a core risk management strategy in private credit, not a luxury.

Stress Testing Risk: The final hidden risk is insufficient stress testing. Private credit is a downside-first discipline. Lenders must imagine scenarios borrowers may not anticipate.

Experienced lenders begin by examining how the borrower performed through past economic cycles — financial crises, industry downturns and liquidity shocks. This historical perspective reveals how resilient the cash flow truly is.

Forward-looking stresses are equally critical. What if revenue drops sharply? What if collateral values reset lower? What if refinancing appetite slows? What if working capital needs rise? The purpose is not predicting the exact scenario, but ensuring the structure withstands severe pressure while protecting principal.

A structure that survives stress is a structure that protects investors.

Private credit can be a powerful and resilient financing solution, but only when risks are understood early and mitigated through strong structuring, conservative underwriting and rigorous due diligence. As Thailand’s market expands, the most successful participants will not be those who focus on high yield, but those who understand risk deeply, prepare for it and structure against it.

Rewin Pataibunlue is a Founding Partner and Group CEO at PrimeStreet Group, an investment banking, strategic management consulting and alternative fund management firm based in Bangkok. This is the third in a five-part series.