Global demand for private credit continues to accelerate, supported by long-term commitments from pension funds, insurers, sovereign wealth funds and the world’s wealthiest families. This momentum is not a short-term reaction to high interest rates, but a reflection of deeper structural changes in global capital markets.

As interest in private credit in Thailand grows, understanding the true drivers of demand is increasingly important for investors, corporate borrowers and policymakers.

A structural shift became clearer in mid-2024, when major central banks, including the US Federal Reserve and the European Central Bank, began easing monetary policy after two years of aggressive tightening. Many investors questioned whether the appeal of private credit would fade alongside falling benchmark rates. Yet data showed the opposite.

According to the Global Private Debt Report 2025 from the alternative asset market data provider Preqin, private-credit assets reached roughly US$2.3 trillion, almost five times their size a decade earlier. This expansion confirms that private credit has moved far beyond its “alternative” status and has become a core component of the global institutional investment landscape.

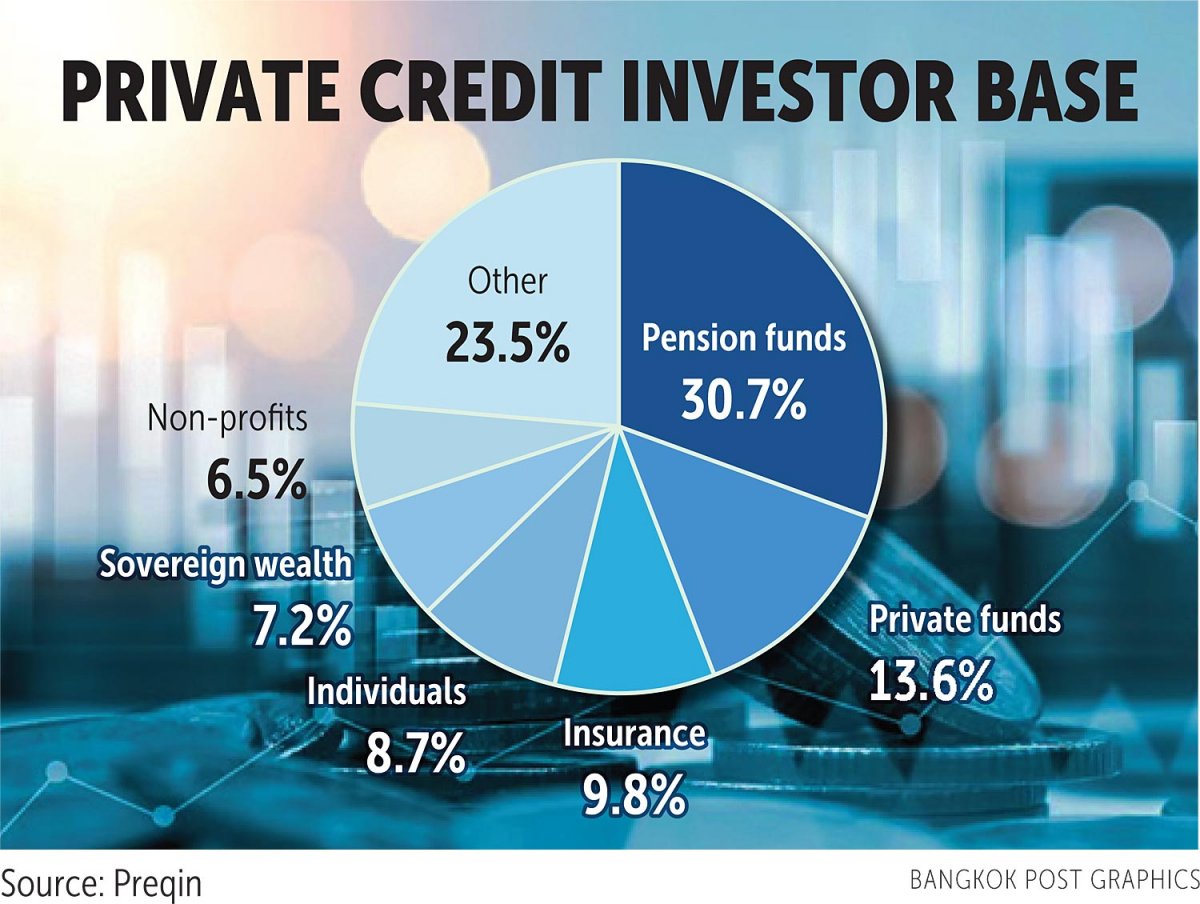

Among all investor classes, pension funds remain the most dependable and influential force behind the growth of private credit. Research from the Federal Reserve highlights that pensions account for a substantial share of global commitments. Leading institutions such as Canada Pension Plan Investment Board, Ontario Teachers’ Pension Plan and CalPERS (California Public Employees’ Retirement System) have steadily increased allocations.

Their interest is driven not by short-term yields, but by structural features that meet long-dated obligations: predictable income, contractual cash flows, strong collateral backing and lower mark-to-market volatility compared with public markets. These qualities make private credit a natural match for pension funds seeking stability across multiple economic cycles.

APPEAL TO INSURERS

Insurance companies represent another key pillar of global private-credit demand. Insurers face a dual challenge: generating reliable income while managing capital requirements under solvency rules. This has led many to favour investment-grade private credit, particularly lending backed by strong corporate or infrastructure assets.

These facilities provide dependable cash-flow visibility and, in several regulatory regimes, more favourable capital treatment than unrated or lower-rated assets, while also supporting better asset–liability duration matching. As a result, private credit has become an increasingly attractive fixed-income alternative for insurers across Europe, the Middle East and Asia.

Sovereign wealth funds have also expanded aggressively into private credit. Institutions such as GIC and Temasek in Singapore, Abu Dhabi Investment Authority and Saudi Arabia’s Public Investment Fund now invest across corporate direct lending, infrastructure credit and asset-backed strategies. Temasek’s launch of a dedicated private-credit platform in 2025 reflects growing conviction in the long-term sustainability of the asset class.

For sovereign funds, private credit offers diversification, contractual returns and the ability to deploy substantial capital efficiently.

Family offices and ultra-high-net-worth investors, meanwhile, are among the fastest-growing groups in private credit. Surveys by global private banks show that allocations have nearly doubled in recent years.

For many Asian family offices, private credit feels familiar because it resembles secured lending and asset-backed financing they have used for decades — except now it is supported by institutional underwriting, diversification and stronger governance.

SCALING UP

To meet rising demand, global private-credit managers have significantly expanded their platforms. Many have launched strategies tailored for pensions, insurers and sovereign funds, emphasising seniority, collateral strength, disciplined covenants and transparent reporting.

Innovation has also accelerated. Evergreen structures, semi-liquid vehicles and feeder-master arrangements are making institutional-grade private credit accessible to a broader investor base without compromising underwriting standards.

Thailand is becoming increasingly connected to these global trends through feeder funds — vehicles managed by licensed Thai asset managers that invest directly in offshore master funds run by leading international private-credit platforms.

Minimum investments typically range from one to ten million baht, offering affluent investors and family offices regulated access to global private-credit portfolios.

Demand in Thailand has risen sharply, particularly among investors seeking stable income, strong downside protection and alternatives to a volatile domestic bond and equity market.

For Thai insurers, certain investment-grade private-credit strategies may also align well with risk-based capital frameworks, making them a capital-efficient complement to traditional fixed-income assets.

Some observers worry about spread compression or weaker underwriting in parts of the market. These concerns primarily relate to highly leveraged or covenant-lite segments, not to senior secured or investment-grade private credit, which dominates institutional portfolios.

This segment continues to be defined by robust collateral coverage, disciplined structures and active monitoring. These features have helped private credit perform resiliently across multiple interest-rate and economic cycles.

As Thailand deepens its engagement with global private credit, the asset class is transitioning from a niche alternative into a core building block of sophisticated Thai investment portfolios.

The long-term drivers — pensions, insurers, sovereign funds and family offices — suggest that private credit momentum will remain strong, even as global monetary conditions evolve.

PrimeStreet Group believes that private credit will continue to play a critical role in Thailand’s investment landscape, particularly as corporates seek more flexible, collateral-backed financing solutions.

Structurally sound, senior secured private credit, supported by disciplined underwriting, active monitoring and proper risk management should remain resilient across rate cycles and will increasingly serve as a stable anchor allocation for Thai investors.

Rewin Pataibunlue is a Founding Partner and Group CEO at PrimeStreet Group, an investment banking, strategic management consulting and alternative fund management firm based in Bangkok. This is the second in a three-part series.